Producer Price Inflation (PPI)

-

PPI inflation (m/m): actual 0,5% (forecast 1.1%, previous 0.7%)

-

Core PPI inflation (m/m): actual 0.1% (forecast 0.5%, previous 0.5%)

-

PPI inflation (y/y): actual 4% (forecast 4.6%, previous 3.4%)

-

Core PPI inflation (y/y): actual 3,8% (forecast 4.2%, previous 3.9%)

Why is this data important?

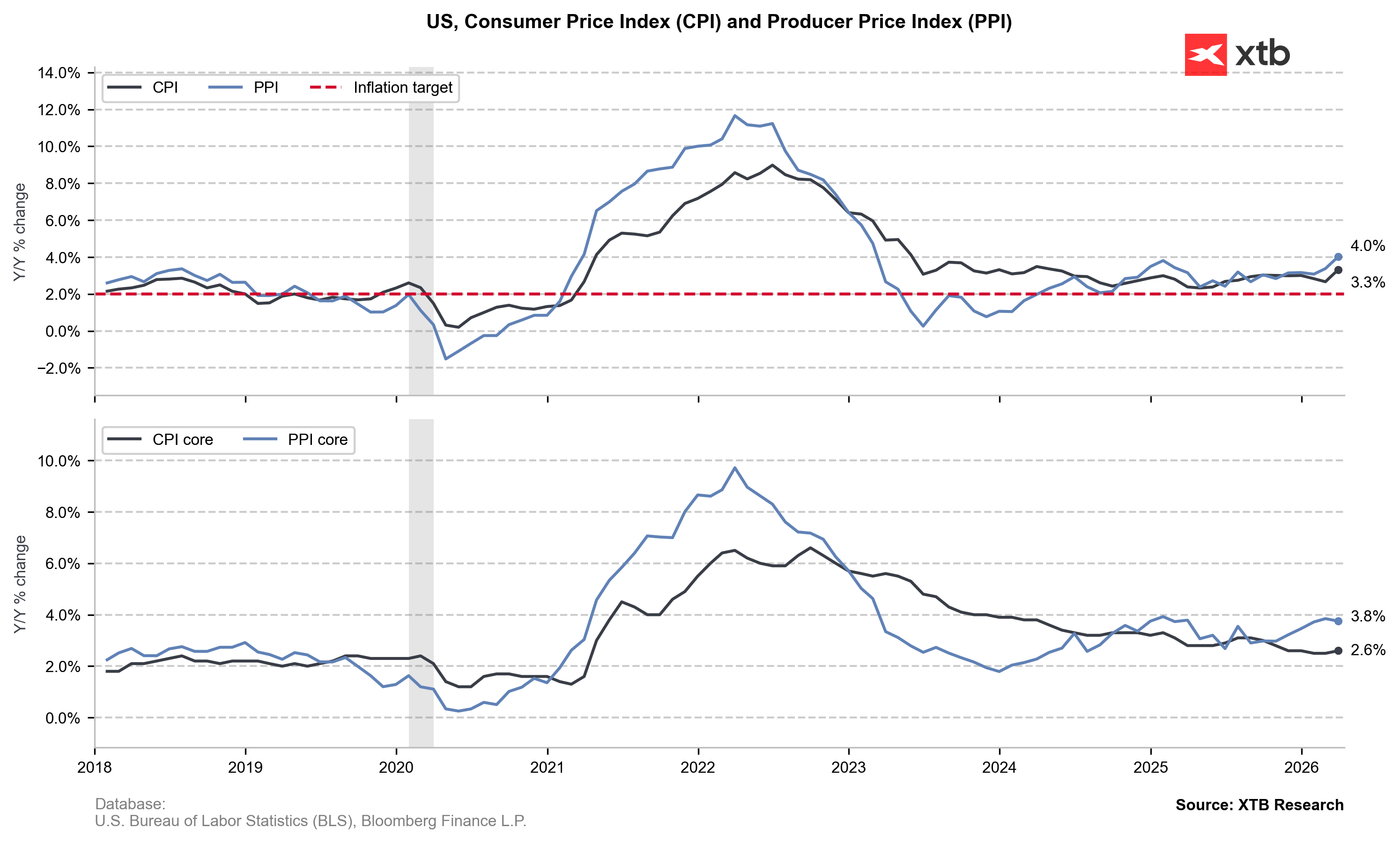

Producer Price Inflation (PPI) measures changes in the prices of goods at the producer level, before they reach consumers. It is one of the key leading indicators of consumer inflation (CPI), as rising production costs are often passed on to end consumers.

An increase in PPI suggests rising cost pressure in the economy, which may lead to higher inflation in the future. On the other hand, a weaker reading indicates lower price pressure and may give the central bank more room for a more accommodative monetary policy. Core PPI is particularly important, as it excludes volatile components such as energy and food, providing a more stable view of underlying price trends.

This report has a significant impact on financial markets. A stronger than expected rise in PPI can support the US dollar and push bond yields higher due to expectations of higher interest rates, while weaker data may have the opposite effect.

Current Data

Producer Price Inflation (PPI) in the US came in clearly weaker than expected, signaling a slowdown in producer-level price pressures.

PPI inflation in monthly terms rose by 0.5%, which is significantly below the forecast of 1.1% and also lower than the previous reading of 0.7%. This suggests that price growth at the producer level has cooled considerably in the short term, pointing to easing cost pressures in the economy.

Core PPI inflation on a monthly basis increased by just 0.1%, also well below the forecast of 0.5% and unchanged from the previous reading of 0.5%. This is an important signal that underlying inflation pressures are weakening even after stripping out more volatile components such as food and energy.

In year-on-year terms, PPI inflation stands at 4.0%, below expectations of 4.6% but above the previous reading of 3.4%. This indicates that while annual price growth remains elevated, the momentum is slowing compared to earlier periods.

Core PPI inflation year-on-year came in at 3.8%, slightly below the forecast of 4.2% and just under the previous 3.9%, reinforcing the view that underlying inflationary pressures are gradually easing.

Overall, the data points to weaker-than-expected producer inflation, which may reduce concerns about persistent cost-driven inflation and could be interpreted as a more dovish signal for monetary policy. In a market context, such a report can weigh on the US dollar and support equities, as it increases expectations that the Federal Reserve has less pressure to maintain a restrictive stance.

Source: xStation5

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.

Source link